It's not about the house. It's about what nobody told them before they bought it.

A statistic stopped me cold this week.

I was watching a video from Nicole Rueth — one of my most trusted lender partners and a woman who has sat across from thousands of families at the most important financial decision of their lives — and she shared a survey finding that genuinely rattled me:

28% of homeowners want to go back to renting.

Not because they bought the wrong house. Because nobody prepared them for what owning one actually costs.

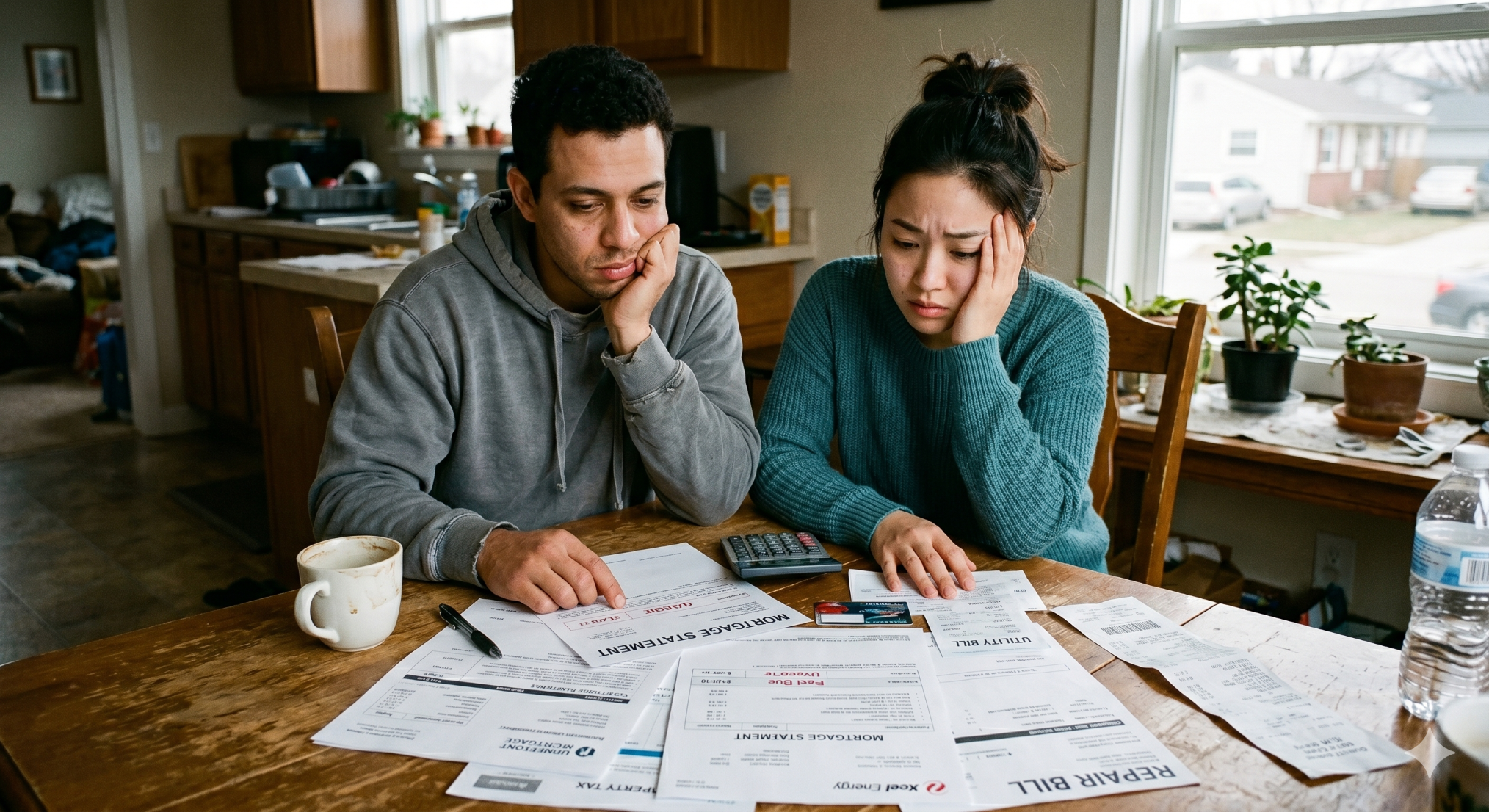

Nearly half said they spent more than they expected. Nine out of ten agreed the true cost of homeownership was higher than they anticipated. And one in five — one in five — said they couldn't cover a $500 repair without putting it on a credit card.

I sat with that for a minute. Because I have nine grandchildren I am actively coaching toward homeownership. I believe in it completely — not as a transaction, but as a foundation. And this statistic isn't an argument against buying. As Nicole put it so well: it's an argument for doing it right.

So let me tell you what "doing it right" actually looks like. And let me show you the tool I built specifically so my buyers never end up in that 28%.

This Is a Preparation Problem. Not a Homeownership Problem.

Here's what the survey doesn't tell you: the 28% who want to go back to renting didn't make a bad decision by buying a home. They made a bad decision by buying without knowing what they were actually committing to.

Nicole said something in her video that I haven't stopped thinking about:

"The people who love homeownership long term are not luckier than the people who regret it. They're just more prepared."

That is exactly right. And it's exactly where most buyers — even financially solid, well-intentioned buyers — get left behind. Not because they can't afford it. Because nobody sat them down before the excitement took over and walked them through the full picture.

That's the conversation a lot of agents and lenders leave out. It's the conversation I refuse to skip.

The Real Number Nobody Talks About

Here's what homeownership actually costs, on average, beyond the mortgage payment:

$22,000 a year. That's $1,800 a month in property taxes, insurance, utilities, maintenance, and repairs — costs that most buyers never fully factor in when they're sitting at the kitchen table trying to decide what they can afford.

Property taxes will rise as home values rise. Insurance costs have surged in many markets. And the roof, the HVAC, the water heater, the plumbing — those aren't "if" questions. They're "when" questions. The only variable is whether you're ready when they happen.

This is not meant to scare you. It's meant to prepare you. Because the buyers who walk into homeownership with eyes wide open — who know their full number, not just their mortgage payment — are the ones who build equity, build confidence, and never look back.

Four Things That Separate Buyers Who Thrive from Buyers Who Regret It

Nicole breaks this down into four pillars, and I've built my entire buyer process around them.

1. Know your real number before you fall in love with a house. Your mortgage payment is one piece. Add in property taxes, insurance, utilities, and 1% of the home's value annually for maintenance and reserves. That is your real monthly number. If that number doesn't work, the house doesn't work — no matter how much you love the kitchen.

2. Understand what you're actually buying — not just the square footage. How old is the roof? What's the remaining life on the HVAC? What about the water heater, the electrical panel, the plumbing? Is there a well or a septic system? These questions feel uncomfortable when you're excited about a home. But they are the questions that protect you after you close. Ask for 12 months of seller utility bills. Request a thorough inspection. Know what you're inheriting.

3. Have reserves before you close. Down payment and closing costs get all the attention — but your emergency fund needs to stay intact after you move in. The goal is three to six months of total housing costs sitting untouched before you buy. If you're not there yet, have a plan to get there. Because something will happen. The question is just whether you're ready when it does.

4. Buy below your approval amount. Your approval number is a ceiling. Not a target. The homeowners who enjoy homeownership long term — who never feel stretched, never feel stressed, never wish they'd kept renting — are almost always the ones who bought a home that fit their life, not one that consumed it.

The Tool I Built So My Buyers Know Before They Buy

Here's where I want to tell you about something I created specifically for this problem.

It's called the Home Payment Comfort Index™ — and it lives at comfort.carliplummer.com.

The bank will tell you what you qualify for. The Comfort Index tells you what will actually feel sustainable — month after month, year after year, through income dips, big repairs, and expensive seasons of life.

It's a 10-question assessment that walks you through the things most lenders never ask: How do you feel at the end of the month right now? If your housing payment increased, what would have to give? How confident are you in handling costs beyond the mortgage? If your income dipped for a few months, what does your cushion look like? If you were approved for more than feels comfortable, would you stay within your own range?

Your responses generate a Comfort Score out of 50 — with a clear picture of whether you're in your comfort zone, close to it, or outside it — for any payment amount you want to model.

This isn't a loan qualification tool. It's a clarity tool. And it's the conversation I have with every buyer before we ever look at a single house.

Because here's what I've learned after years in this business and nine grandchildren I'm personally coaching toward homeownership: the fear most buyers have isn't really about the market. It's about not knowing whether they'll be okay on the other side of the decision. The Comfort Index answers that question before it becomes a regret.

What I Know About Homeownership Done Right

Nicole has 60 investment doors and watched her three children buy their first homes at 21. She also lost nearly $20,000 in nine months on a home she didn't fully understand. She'll tell you both things are true — and both things matter.

I think about my grandchildren when I hear that. Every single one of them. I want them to build wealth through real estate. I want them to have the optionality that homeownership creates — the ability to pull equity when opportunity knocks, to build a foundation that renting simply cannot provide. But I want them to go in prepared. Not stretched. Not surprised. Not in that 28%.

That's exactly what I want for you too.

The 28% who regret it didn't fail at homeownership. They just went in without the full picture — and without someone who stopped them before the excitement took over and had the honest conversation first.

I am that person. That's what I do, every single time.

Ready to Find Out Where You Stand?

Take the Home Payment Comfort Index™ — it takes about three minutes, and it will tell you more about your real readiness than any pre-approval letter will.

Find your Comfort Score → comfort.carliplummer.com

And if you want a real conversation about what the path to homeownership actually looks like for your situation — with a buyer's agent and a lender partner who will both tell you the truth — that starts here:

Start the conversation → start.carliplummer.com

Carli Plummer is a buyer's agent serving the Denver Metro Area. She works with first-time buyers, move-up buyers, and anyone who wants to walk into homeownership prepared — not surprised.

**Reprinted with permission from Nicole Rueth.

Check out this article next